Randomly Rudimentary Life Stuff

Learning to live authentically, and not settling for substitutes or counterfeits, and sharing those thoughts

The Loan That Opened a Door—And the System That Shut It for Others

By Lonnie King

In September of 1979, I arrived at Texas A&M University as a wide-eyed freshman journalism major. Back then, A&M still had a journalism department—tucked away in the Reed-McDonald Building—and I spent more than a few afternoons wandering its halls, hoping to eventually land a spot on the writing staff of the campus daily paper, The Battalion.

I owned a little version of an IBM Selectric typewriter—a clunky, glorious beast that made me feel like a real writer every time I hit the keys. Except for my contributions to my high school newspaper, I wasn’t published yet, but I was serious.

And I was hopeful.

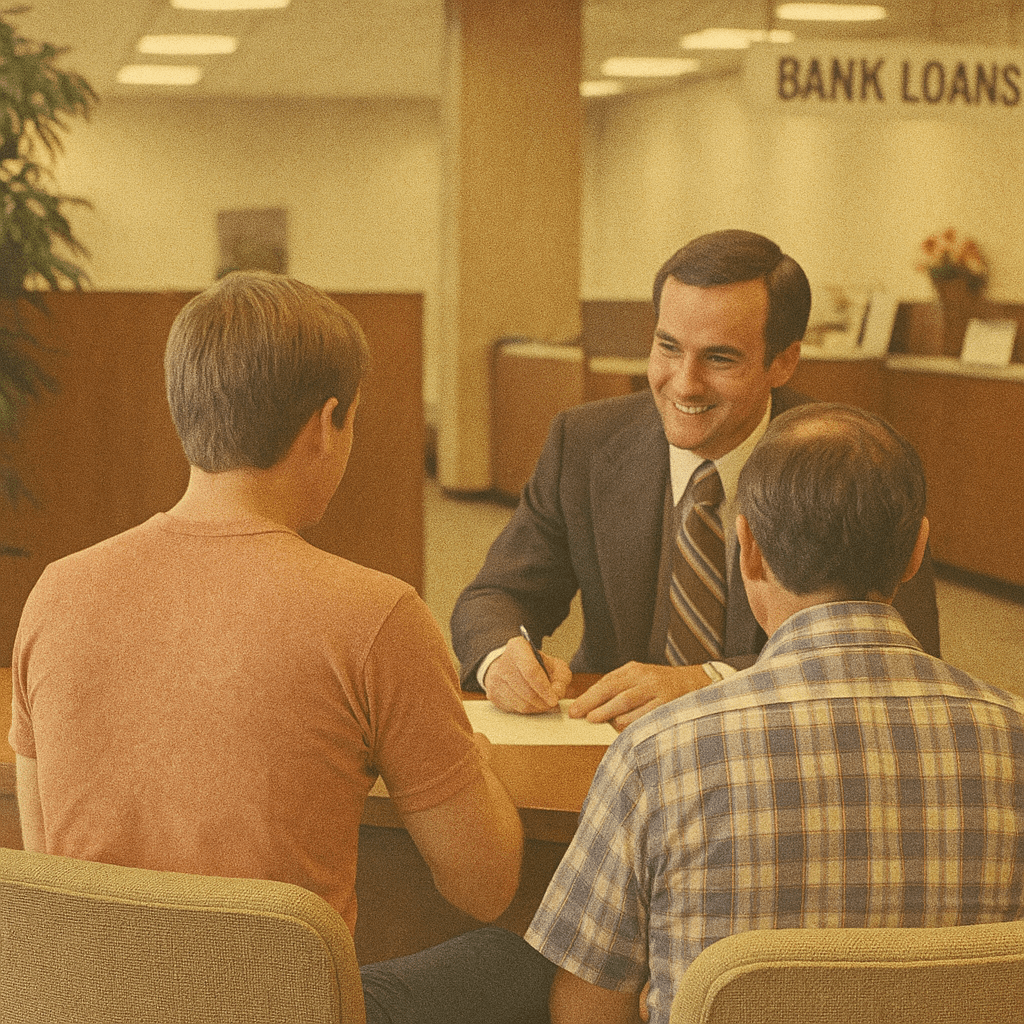

I also had a $2,500 loan from Texas Commerce Bank—secured with my dad’s help—and that one loan covered two full semesters of college. Tuition, housing, books, food, and even the occasional Whataburger run or tank of gas for a quick weekend road trip. All of it.

Campus life felt different then. Smaller. Friendlier. Maybe it’s just the soft-focus lens of memory, but there was less arrogance, less edge. People held doors for each other. You could walk across campus and actually make eye contact without it feeling like a power play.

The A&M of today, with its sprawling enrollment and powerhouse SEC status, feels like a different school entirely—more prestigious, maybe. But also more impersonal.

Back in ’79, I was what they called an “Aggie Fish”—a freshman trying to find his way in a place that still echoed its all-male military roots, even as it worked to welcome women and civilian students into the fold. The education was real, and the cost? Surprisingly manageable. Even for a middle-class family like mine.

I don’t remember feeling like I was buying a future. I just remember feeling like I was getting started.

When a Loan Became a Life Sentence

Today, a student at Texas A&M would be laughed out of the financial aid office with only $2,500 to spend. That might not even cover a month of expenses. Tuition alone is more than ten times what it was back then, and housing, fees, and food keep rising too.

Back then, it wasn’t just loans that made college attainable—it was the basic math of work and wages.

In 1978, the federal minimum wage was $2.65/hour. A student working 40 hours a week for 13 weeks over the summer would earn about $1,378—enough to pay for the average in-state tuition of $1,369 at a four-year public university. One summer job could cover a year of classes.

That sounds almost mythical now.

Each of my four kids has student loans—federally insured, but heavy all the same. My wife and I even took out Parent PLUS loans to help them bridge the gap, with the understanding they’d help repay them once they started earning income.

We did what parents are supposed to do: support our kids’ education. But what we all walked into was a trap that wasn’t fully disclosed. One generation borrowed a few thousand dollars to unlock opportunity. The next borrowed tens of thousands just to access the minimum credential employers now demand.

And that’s where the real twist comes in.

The System That Created the Problem Now Refuses to Solve It

A big part of the reason college became unaffordable is because public investment in higher education declined sharply over the decades following the 1970s. State governments shifted the cost burden to students.

Meanwhile, federally-backed student loans began to make it easy for colleges to raise costs in response to that declining public investment—because they knew the government would foot the gaudy bill upfront and, if necessary, take on the role of debt collector later on.

For colleges and universities, it became a cash grab—and a win/win. Students could claim degrees from respected institutions without directly viewing them as overbearing creditors later.

And for the federal government, it was just bad policy, layered over bad incentives, baked into a toxic stew of public neglect and private profiteering.

Yet, today, when anyone dares to propose student loan forgiveness, or even modest relief for borrowers, we’re told it’s immoral. That it rewards laziness. That it’s unfair to people who paid their debts.

But what about the government’s role in jacking up the cost in the first place? What about the employers who now demand degrees for jobs that have nothing to do with higher education? What about the families—like mine—who weren’t irresponsible or extravagant, just hopeful?

Hopeful that maybe, like in 1979, a loan could still open a door.

A Cycle We Can’t Seem to Break

We’ve normalized a system where teenagers take on mortgage-sized debt to get a piece of paper that might qualify them to earn an entry-level wage. Sit with that for a minute.

It’s a system where parents in their 50s and 60s are still paying off loans that weren’t even for their own education. Where employers use college degrees as lazy filters, and politicians talk about the cost of forgiveness but not the cost of exploitation.

This isn’t just about economics. It’s about ethics. It’s about a society that tells you you have to go to college to matter, then makes you pay for the privilege for the next 20 years—unless you default, go bankrupt, or die trying.

And yes, I know that sounds dramatic. But for many families, it’s true.

Final Thought

I didn’t know it at the time, but the loan I took out in 1979 changed my life—in a good way.

It paid for a year that lit a fire in me. That first year at A&M deepened what was already a budding obsession with journalism. It placed me in classrooms where I began to understand the role of a journalist not as a spin doctor, but as a truth-seeker.

It gave me the tools to start learning how to write, how to communicate, how to think critically.

I don’t know if I would have gone to college at all without that loan—but I do know that the education it made possible helped shape me into the person I am today.

I believe in higher education. I believe in a system that fosters ambition, that encourages people to ask questions and seek truth and find their voice.

I just don’t believe it should come at the cost of a lifetime of debt.

For a lot of families today, loans don’t feel like a launchpad. They feel like a life sentence.

We built a system that nudges people into debt, then blames them for being there. We’re told education is the path to opportunity. But somewhere along the way, that path became a toll road with no exit.

And those of us who traveled it early on? We can’t just ignore the roadblocks now, just because we made it through when the tolls were cheaper.